Consumer digital payment spending reached nearly $50 trillion globally in 2024, with digital wallets accounting for over $41 trillion of that volume. The payment gateway market is expanding in parallel: valued at $32 billion in 2023, projected to exceed $37 billion in 2024 at a 17% compound annual growth rate. Whether you need to develop payment gateway infrastructure from scratch or add a new payment layer to an existing product, early decisions define the cost and capability of everything downstream.

For SaaS platforms, marketplaces, and eCommerce businesses, knowing how to get a payment gateway that fits your product is both a technical and a strategic question: fee structures, customization limits, and data ownership all depend on the path you choose.

This guide walks through how to create a payment gateway for website and app environments, explains the distinction between a gateway and a payment processor, presents a reference architecture, and covers what it actually costs to build and maintain one in production.

What Is a Payment Processor?

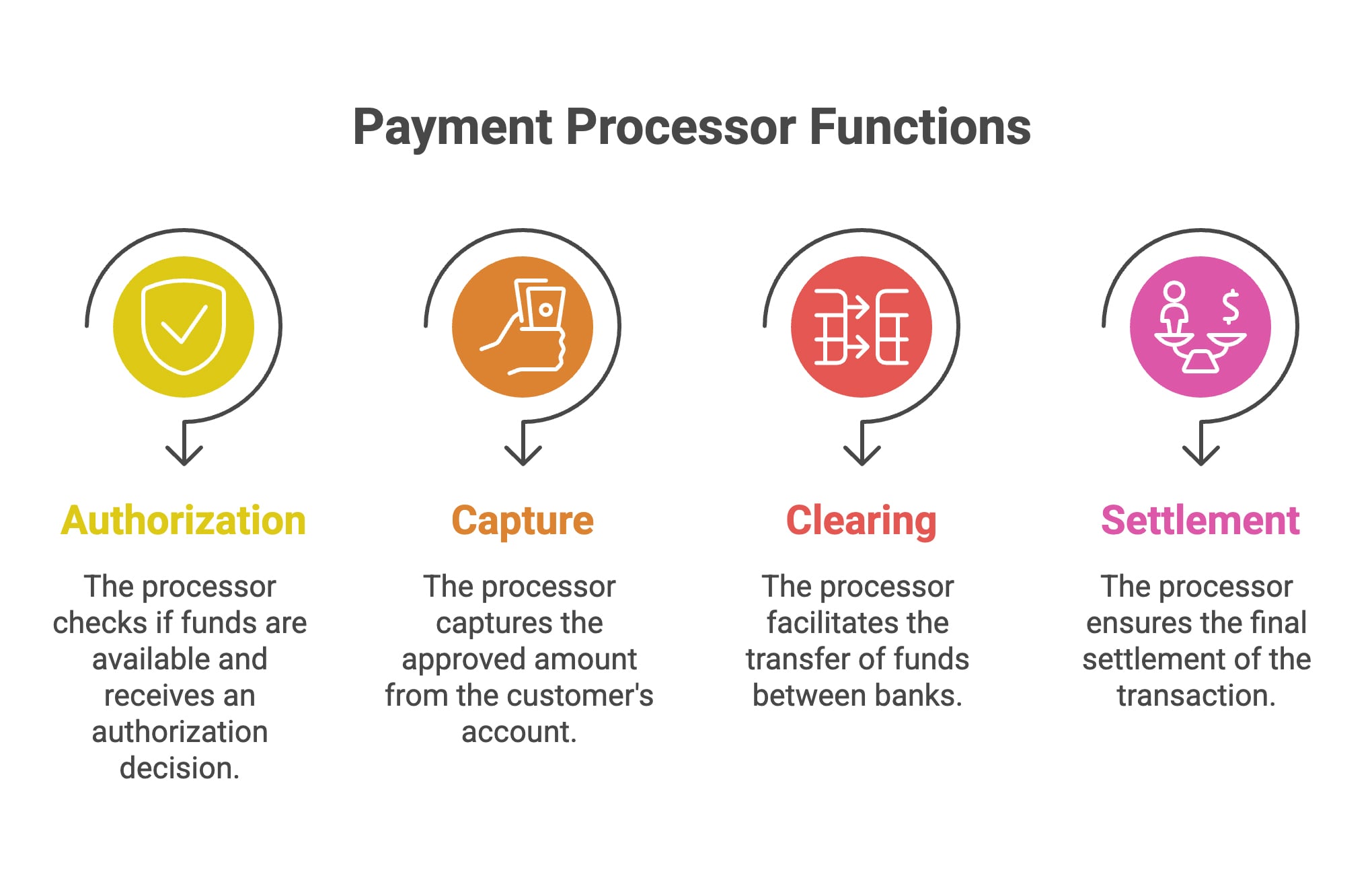

A payment processor is the engine that moves money between accounts. When a customer completes a purchase, the processor communicates with the customer’s issuing bank, checks whether funds are available, receives an authorization decision, and transfers the approved amount to the merchant’s acquiring bank. It handles the core mechanics of the transaction: authorization, capture, clearing, and settlement.

The payment processor operates largely out of sight. A user buying a SaaS subscription sees a checkout form; what they do not see is the processor sending an authorization request to Visa or Mastercard, routing it to the issuing bank, receiving an approval code, and queuing the transaction for settlement. This entire sequence typically completes in two to three seconds.

The key distinction from a payment gateway is scope. A processor handles the financial movement of funds between institutions. A gateway handles the front-end capture and routing of payment data before it ever reaches the processor. The two are distinct roles, even when a single provider bundles both into one product. Stripe and Adyen are the most common examples of combined gateway-and-processor platforms.

For businesses evaluating whether to build their own infrastructure, understanding this split matters practically. You can build a proprietary gateway that encrypts and routes payment data while still relying on an established processor for clearing and settlement. Many fintech products are structured exactly this way: a custom front-end payment experience with third-party clearing and settlement handling the movement of funds on the back end. This approach is often the right starting point for how to create your own payment gateway without taking on the full complexity of becoming a licensed payment processor at the same time.

What Is a Payment Gateway?

A payment gateway is the software layer that sits between your customer and the financial institutions that process their payment. When a user enters card details or initiates a bank transfer on your website or app, the gateway captures that data, encrypts it, authenticates the request, and routes it to the appropriate payment processor or acquiring bank. It is the entry point of every digital transaction running through your platform.

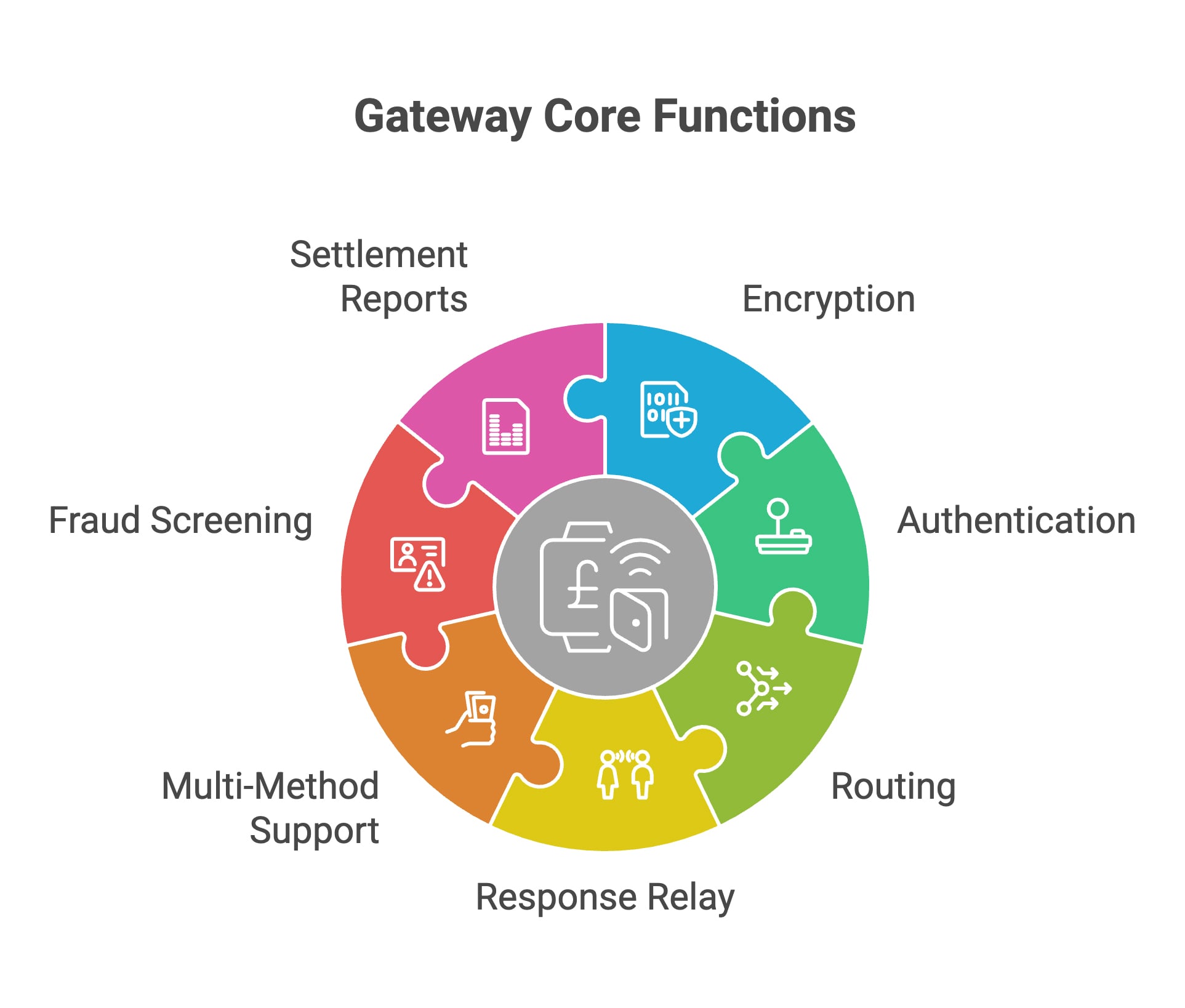

The core functions of a gateway include:

- Encryption of sensitive payment data at the point of entry using TLS and tokenization

- Authentication of the transaction, including 3D Secure checks where applicable

- Routing the payment request to the correct processor or acquiring bank

- Receiving and relaying the authorization response back to the merchant and customer

- Supporting multiple payment methods: cards, digital wallets, bank transfers, and local payment schemes

- Fraud screening and risk scoring before the transaction is submitted for authorization

- Providing settlement reports and reconciliation data to the merchant’s finance systems

Some providers combine gateway and processor functions in a single integrated product. This simplifies initial integration but removes control. When gateway and processor are the same vendor, you are bound by their routing logic, their fee structure, and their uptime. Building a proprietary gateway means decoupling these layers and owning the rules that govern how transactions flow through your infrastructure.

Knowing how to make a payment gateway that performs well in production requires making security and routing decisions at the architecture level, before development begins. Retroactively adding these to a running system is technically possible but carries significant cost and risk.

Why Build Your Own Gateway?

There are several business-driven reasons to set up your own gateway rather than renting access to a third-party system. The most common ones that surface in real product decisions are:

Control over conversion and UX. Third-party gateways redirect users or inject iframes that you cannot fully style, instrument, or A/B test. A custom gateway keeps the entire checkout flow within your product, where every element that affects conversion is yours to control and optimize.

Multi-product and multi-region coverage. A single proprietary gateway can serve several products or markets from one integration layer, eliminating the need to manage separate vendor contracts and configurations for each geography or product line.

Smart routing and provider redundancy. Custom gateways implement least-cost routing and automatic failover between payment processors, reducing both transaction costs and exposure to any single provider’s downtime.

Data ownership. Every authorization, decline, and fraud signal generated by your gateway belongs to you. Over time, this data becomes the foundation for routing optimization, fraud modeling, and finance reconciliation.

How Payment Systems Work

A payment gateway and a payment processor each play distinct roles, but they operate as part of the same transaction chain. Understanding where they intersect is essential before setting up a payment gateway or deciding how to build a payment gateway for your website or platform.

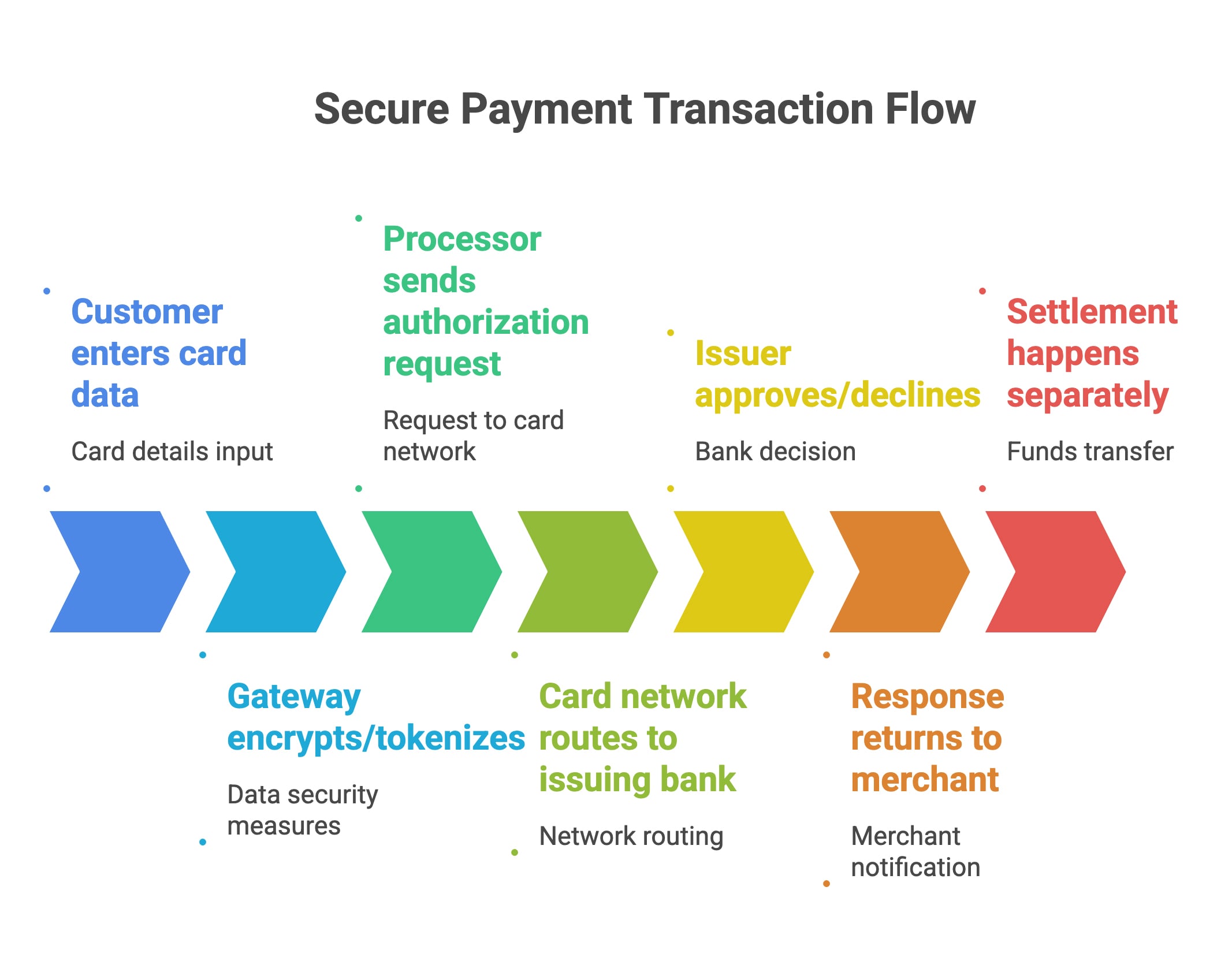

When a customer initiates a payment, the sequence unfolds as follows. The gateway captures the payment data, typically a card number, expiry, and CVV, encrypts it immediately using TLS, and replaces the raw card data with a unique token. This tokenized request is submitted to the payment processor. The processor forwards an authorization request to the relevant card network, Visa or Mastercard, which routes it to the customer’s issuing bank. The issuing bank checks available funds, applies its fraud rules, and returns an approval or decline code. The card network relays the response to the processor, which passes it to the gateway, which delivers the result to the merchant’s website or app. This full cycle typically completes in under three seconds.

Settlement is a separate, downstream process. Once a transaction is authorized, the acquiring bank batches approved transactions and settles funds to the merchant account, typically within one to three business days. The gateway generates a settlement report used for reconciliation against internal records.

Where gateway and processor overlap is in integrated platforms like Stripe or Adyen, where a single API handles both routing of payment data and movement of funds. In a custom-built architecture these layers are separated. Your proprietary gateway handles front-end data capture, encryption, fraud screening, and routing, while one or more third-party processors handle clearing and settlement. This separation gives you the ability to route different transaction types to different processors based on cost, geography, or authorization rate performance. Knowing how to set up a payment gateway with clean layer separation from the start is what makes this flexibility possible.

Authorization and settlement are separate events. Authorization happens in seconds. Settlement of funds to your account takes one to three business days. Your gateway must handle both flows correctly.

Based on our experience building payment infrastructure for fintech clients, the most common architectural mistake is treating the gateway as a simple pass-through. When a gateway is not designed as a controlled routing layer with its own fraud visibility and fallback logic, it offers no protection against processor failures and no path to cost optimization as volume grows. For the Coinstar digital wallet and crypto trading ecosystem, which required simultaneous integration with payment providers across both fiat and crypto rails, the clean separation of gateway and processor layers was what made the system auditable and extensible at enterprise scale.

Itexus Payment Gateway Architecture Sample

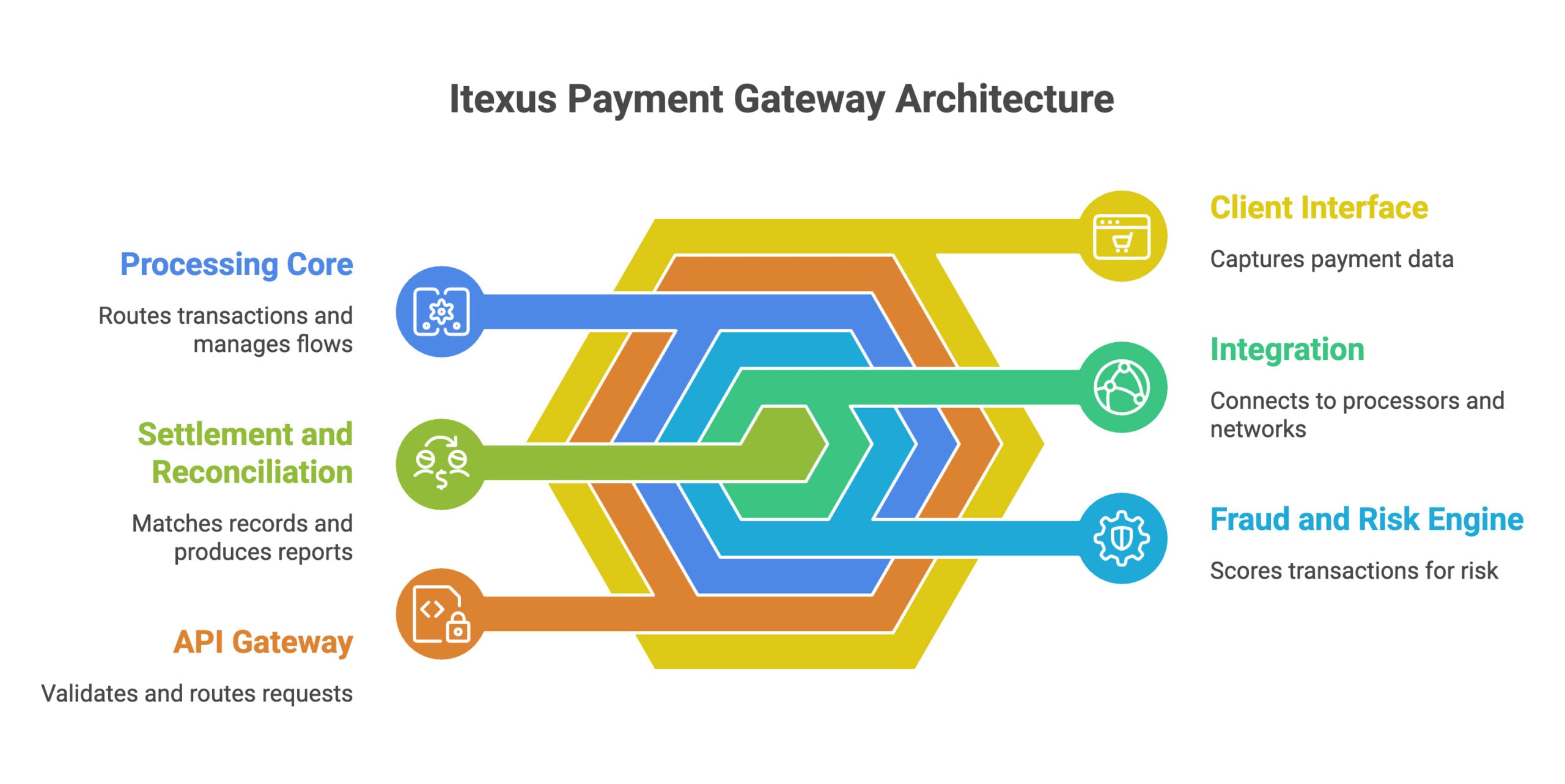

A payment gateway architecture built for production consists of several interconnected layers, each with a defined responsibility. Below is the reference architecture Itexus uses as a starting point for custom gateway development engagements. Understanding this structure also helps teams assess whether open-source components can be used to create your own payment gateway for free in early stages, or whether compliance requirements demand a fully custom build.

At the outermost layer sits the client interface: the checkout form or SDK embedded in the merchant’s website or mobile app. This layer captures payment data and passes it securely to the next layer. No raw card data is stored or logged here.

The API gateway layer receives the encrypted request, validates authentication credentials, applies rate limiting, and routes the request to the processing core. It handles API versioning and maintains a full audit log for compliance and debugging.

The processing core contains the routing logic. It determines which processor or acquiring bank receives each transaction based on currency, card scheme, merchant category, and historical authorization rate. It manages 3D Secure flows and retry logic on soft declines.

The fraud and risk engine runs in parallel. It scores each transaction against rule sets and, in mature implementations, machine learning models. High-risk transactions are flagged or declined before reaching any external system.

The integration layer connects to processors, card networks, and local payment providers via their APIs. Each connection is managed as an independent module, so adding a payment method or replacing a processor does not require core changes. This modularity is what makes it practical to build a payment gateway that evolves with your product.

The settlement and reconciliation layer pulls records from all connected processors, matches them against internal records, and produces settlement reports for downstream finance systems.

How to Create a Payment Gateway: Step by Step

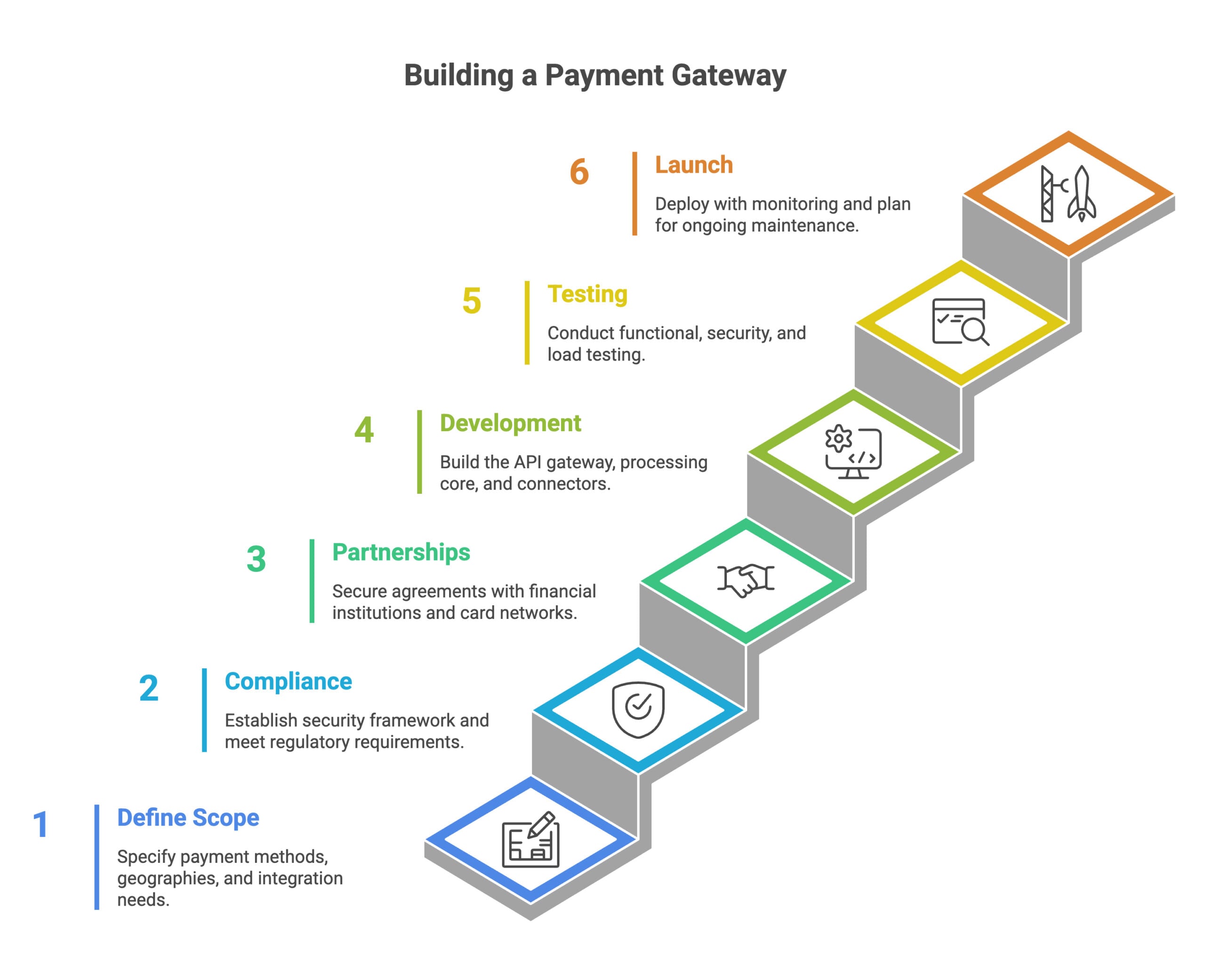

How to create a payment gateway involves six sequential phases. Each phase has dependencies on the one before it, and skipping steps early typically creates expensive rework later. The same plan applies whether you are exploring how to create my own payment gateway as a standalone product or adding a custom layer to an existing platform.

Step 1: Define scope and requirements

Specify which payment methods the gateway must support, which geographies it will serve, what peak transaction volumes it must handle, and how it integrates with your existing systems. This phase produces the technical specification and informs the compliance scope. Decide whether you are building a full proprietary stack or a custom gateway layer routing to third-party processors. For most first-time builds, the latter is the right starting point.

Step 2: Compliance and security architecture

Establish your compliance framework before writing any code. PCI DSS Level 1 certification is required for any system that stores, processes, or transmits cardholder data. In Europe, PSD2 strong customer authentication requirements apply. In the U.S., state money transmission licenses may be required and can reach $500,000 in aggregate fees and reserves. Tokenization approach, encryption standards, and key management decisions must be made at this stage, not retrofitted later.

Step 3: Financial institution partnerships

Acquiring bank agreements and card network certifications are not developer-controlled. These negotiations require compliance evidence, take months, and may involve revenue minimums. Start these conversations in parallel with development. For local payment methods, plan separate agreements with each provider.

Step 4: Software development

Build the API gateway layer, processing core, fraud engine, and integration connectors in sequence. Use sandbox environments for all third-party integrations before connecting to live systems. Working with experienced banking app development companies in the United States that understand payment compliance reduces the time to a production-ready, certifiable architecture significantly.

Step 5: Testing and certification

Run functional testing of each payment flow, security penetration testing, and load testing at projected peak volumes. PCI DSS certification requires formal penetration testing before the audit. Allocate four to six weeks minimum for this phase.

Step 6: Launch and ongoing maintenance

Deploy with full monitoring, alerting, and incident response procedures in place. To build a payment gateway that stays production-grade, plan for ongoing engineering: processor API changes, fraud rule updates, and compliance reviews are recurring requirements. Annual maintenance runs 10% to 20% of the initial build cost. Budget for this before launch, not after.

Benefits of Building Your Own Payment Gateway

The business case for building a custom gateway strengthens as transaction volume grows and product requirements become more specific. The core benefits that matter most in practice are:

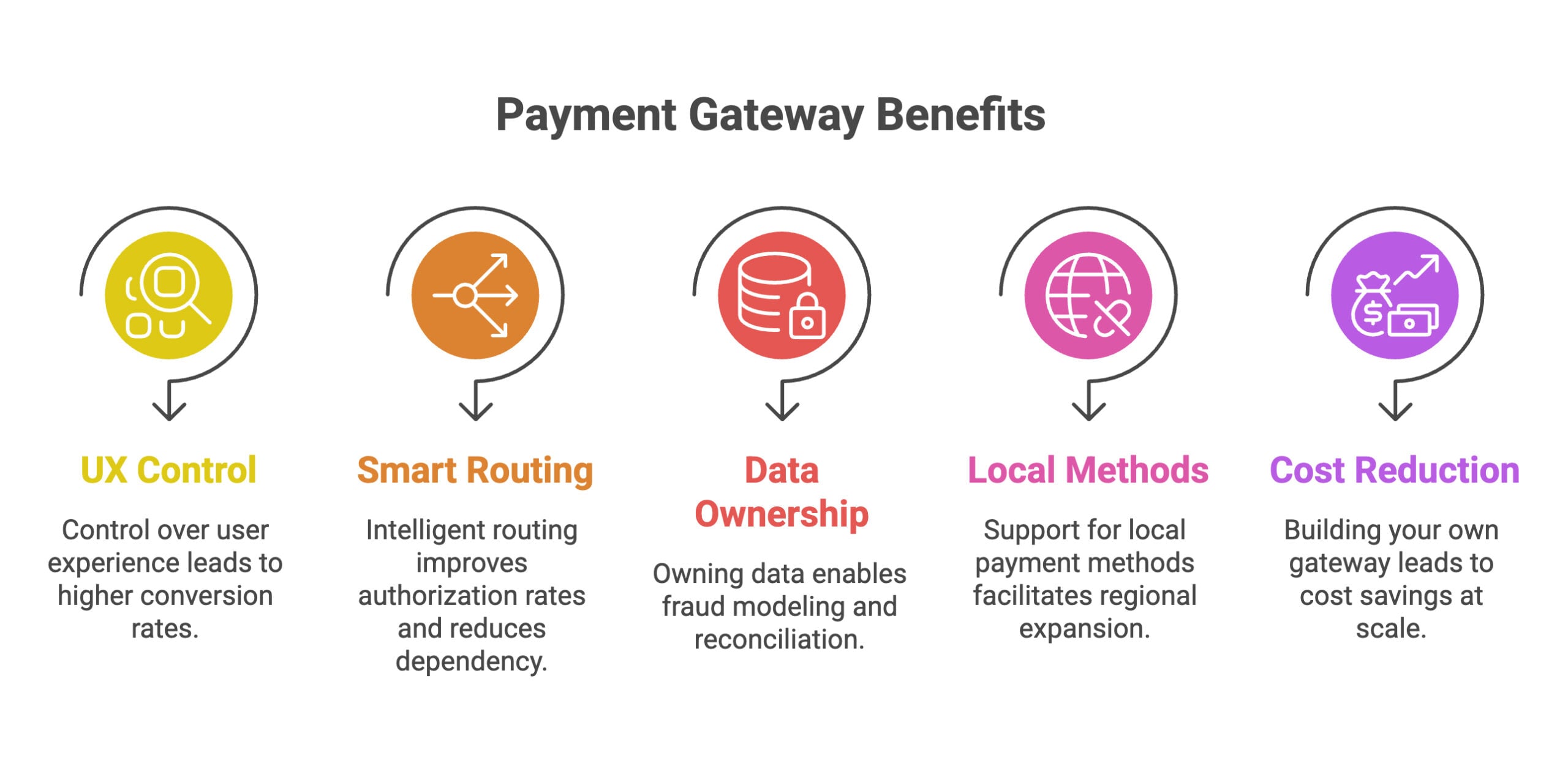

Full ownership of the payment experience. A custom gateway keeps every step of checkout inside your product. You control the UI, the error messages, the retry logic, and the data you capture. This directly affects conversion rates. Redirects and third-party iframes introduce friction that you cannot remove; a native payment experience eliminates it entirely.

Transaction cost reduction at scale. Third-party gateways charge between 0.5% and 3% of transaction value, plus per-transaction fees. At high monthly volume, the difference between a percentage-based gateway fee and a flat per-transaction rate on a custom gateway becomes a significant cost line. High-volume platforms typically recover build costs within 18 to 36 months of going live.

Multi-provider routing and resilience. A custom gateway routes transactions to the processor with the highest authorization rate for a given card type, or fails over automatically when a processor experiences downtime. This optimization is not possible with a single third-party gateway. When Itexus built the Mexico-market mobile e-wallet platform, integrating Stripe alongside local payment rails and a Central Bank virtual card provider, intelligent routing was what allowed the product to maintain 24/7 availability and offer fee-free banking.

Data ownership and reconciliation control. Every transaction that passes through your gateway generates data: authorization rates, decline codes, fraud signals, and settlement timing. Owning this data means building your own analytics, optimizing routing rules over time, and reconciling against your own financial records. For the B2B billing platform Itexus built processing over 100,000 invoices per month via Dwolla and Plaid, this data layer was the foundation of automated reconciliation across multiple payment providers.

Support for local payment methods. Global gateways cover major card schemes reliably. Local methods, including UPI in India, PIX in Brazil, iDEAL in the Netherlands, and BLIK in Poland, require direct integration agreements. A custom gateway gives you a direct path to any payment method your market requires, with no dependency on a third-party provider’s roadmap.

Long-term competitive moat. For payment-native businesses, owning payment infrastructure is a defensible advantage. It compounds over time as routing intelligence and fraud models are built on top of proprietary transaction data. It is harder to replicate than a product feature and increasingly difficult for a competitor to match once the data set matures.

Barriers to Building Your Own Payment Gateway

Building a payment gateway is not a standard software project. The barriers that stop most attempts midway are predictable, and understanding them before you start is the only way to plan around them effectively.

Compliance requirements. PCI DSS Level 1 certification is the baseline for handling cardholder data. Achieving it requires a formal audit by a Qualified Security Assessor, annual penetration testing, quarterly network scans, and ongoing policy enforcement. In the U.S., money transmission licensing varies by state. In Europe, PSD2 adds strong customer authentication obligations. These are permanent operational commitments that require dedicated personnel, external auditors, and recurring budget, every year.

Security complexity. A payment gateway is a high-value target. Encryption, tokenization, key rotation, fraud detection, and anomaly monitoring must be built into the architecture from day one. Security vulnerabilities in payment systems carry regulatory penalties, chargeback liability, and reputational damage that can exceed the cost of the original build. Security is not a feature to add later; it is the foundation.

Technical expertise. Building a production-grade gateway requires specialists in payment protocol standards, cryptography, API design, and financial systems integration. Most product engineering teams do not have this in-house. Assembling the right team, whether through a fintech solution development partner or internal hiring, is one of the first decisions that needs to be right.

PCI DSS Level 1 is not a one-time certification. It requires annual audits, quarterly network scans, and continuous enforcement of security policies. Build the operational budget for this before you build the system.

Maintenance burden. Payment systems require continuous engineering attention after launch. Processor APIs change on their own schedules. Fraud patterns evolve faster than static rule sets. New payment methods need integration agreements. Compliance requirements update at the regulatory level. A gateway that is not actively maintained becomes a liability rather than an asset.

Time and capital. Building an MVP payment gateway typically costs $150,000 to $250,000. A full production system ranges from $200,000 to over $1,000,000 depending on scope. Timeline from planning to first live transaction is typically six to twelve months.

Financial institution partnerships. Acquiring bank agreements and card network certifications are controlled by banks and networks, not by your development team. Negotiating them takes time, requires compliance evidence, and may involve revenue minimums. Starting these conversations before development is complete is essential to avoid a production-ready system waiting on banking approvals.

Cost of Development

The cost to develop a payment gateway depends on scope, team location, and compliance requirements. Based on published benchmarks from Stripe and multiple payment development firms:

- MVP gateway (core card processing, single processor, basic fraud rules, PCI DSS scope): $150,000 to $250,000

- Full production system (multi-processor routing, local payment methods, advanced fraud engine, multi-region compliance): $200,000 to $1,000,000+

- Annual maintenance: typically 10% to 20% of the initial build cost

The largest cost variables are the PCI DSS audit and remediation ($50,000 to $200,000), banking integration setup ($100,000 to $500,000), and team location. Eastern European development rates typically run 40% to 60% lower than U.S.-based teams for equivalent scope, which is why outsourcing to an experienced fintech development firm is a common cost optimization strategy.

The $150,000–$250,000 MVP figure covers a minimum viable gateway. It does not include money transmission licensing, which in the U.S. can reach $500,000 in state-level fees and reserves.

Benefits vs. Barriers at a Glance

Before committing to a build, it helps to see the trade-offs side by side.

| Benefit | Barrier |

| Full control over checkout UX and conversion | Significant upfront engineering investment |

| Cost savings at scale vs. per-transaction fees | PCI DSS Level 1 certification required and ongoing |

| Multi-provider routing improves auth rates and uptime | Technical expertise is narrow and expensive to hire |

| Ownership of all transaction and fraud data | Continuous maintenance required after launch |

| Support for local payment methods globally | Financial institution partnerships take months to establish |

| Long-term competitive moat as data compounds | Money transmission licensing adds cost and complexity in the U.S. |

The decision comes down to volume and strategic intent. For businesses processing high payment volumes where the checkout experience is a core product differentiator, the investment in a custom gateway typically pays off. For businesses at early scale where payment is a commodity function, a third-party gateway is the right starting point.

Closing Thoughts

Building a payment gateway is one of the more consequential infrastructure decisions a payments-oriented business can make. Done well, it delivers control over the user experience, measurable cost savings at scale, resilience through multi-provider routing, and a data asset that compounds in value over time. Done without adequate planning for compliance and security, it becomes an expensive liability.

The path to how to create a payment gateway starts with clarity on scope: which payment methods you need, which geographies you serve, and what transaction volume justifies the investment. It continues through a compliance architecture designed before the first line of code, financial institution relationships initiated early, and a development approach that treats security as a first-class architectural concern.

How to start a payment gateway company or add a custom gateway to an existing product follows the same logic: understand the layers, plan for operational overhead, and build for extensibility from day one. The businesses that execute this well treat the gateway not as a cost center but as a strategic asset. For companies seeking a proven fintech solution development partner for this work, the engagement starts with getting the architecture and compliance scope right before a single line of code is written.