A centralized platform for trading over-the-counter securities that brings holders and investors together, allowing them to bypass intermediaries and trade assets – quickly and easily.

In fintech, positioning matters. In regulated brokerage infrastructure, honest positioning matters even more — because the words a platform uses to describe itself quietly set the bar that regulators, partners, and sophisticated operators will measure it against.

For any regulated trading platform, the infrastructure category defines more than the technical stack — it shapes supervision, recordkeeping, partner responsibilities, and operational risk.

Two of the most commonly confused categories in this space are:

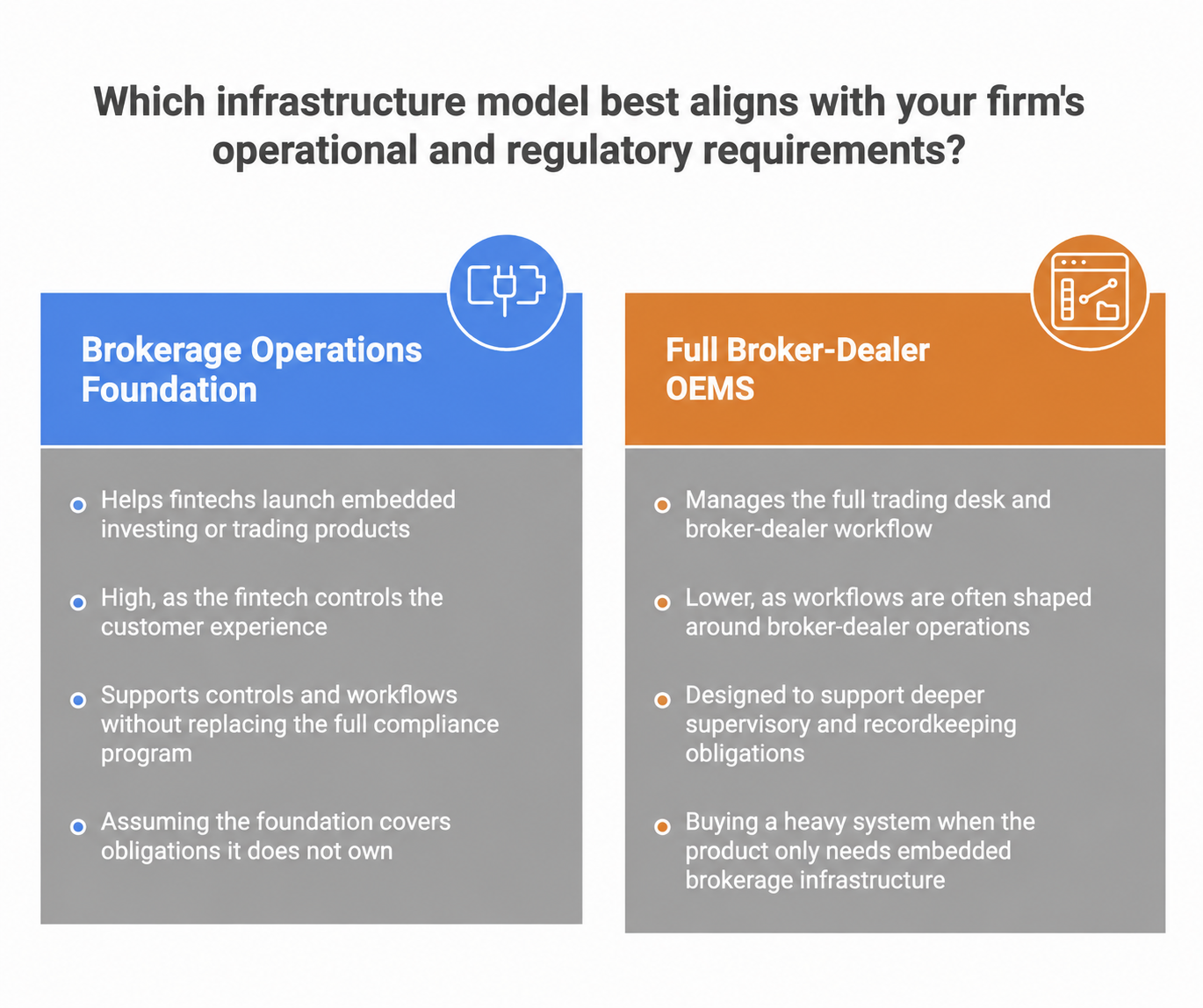

- A brokerage operations foundation — a shared infrastructure layer providing controls, records, funding safety, order-risk primitives, and tenant-scoped supervisory tooling.

- A full broker-dealer Order and Execution Management System (OEMS) — an end-to-end, production-hardened system that covers the full trading and supervisory lifecycle expected of a registered broker-dealer.

These terms often get used interchangeably in marketing. They should not be. Choosing the wrong label has real operational, commercial, and regulatory consequences.

This article breaks down what each category actually is, where each one shines, where each one breaks, and how teams building a regulated trading platform should think about infrastructure positioning.

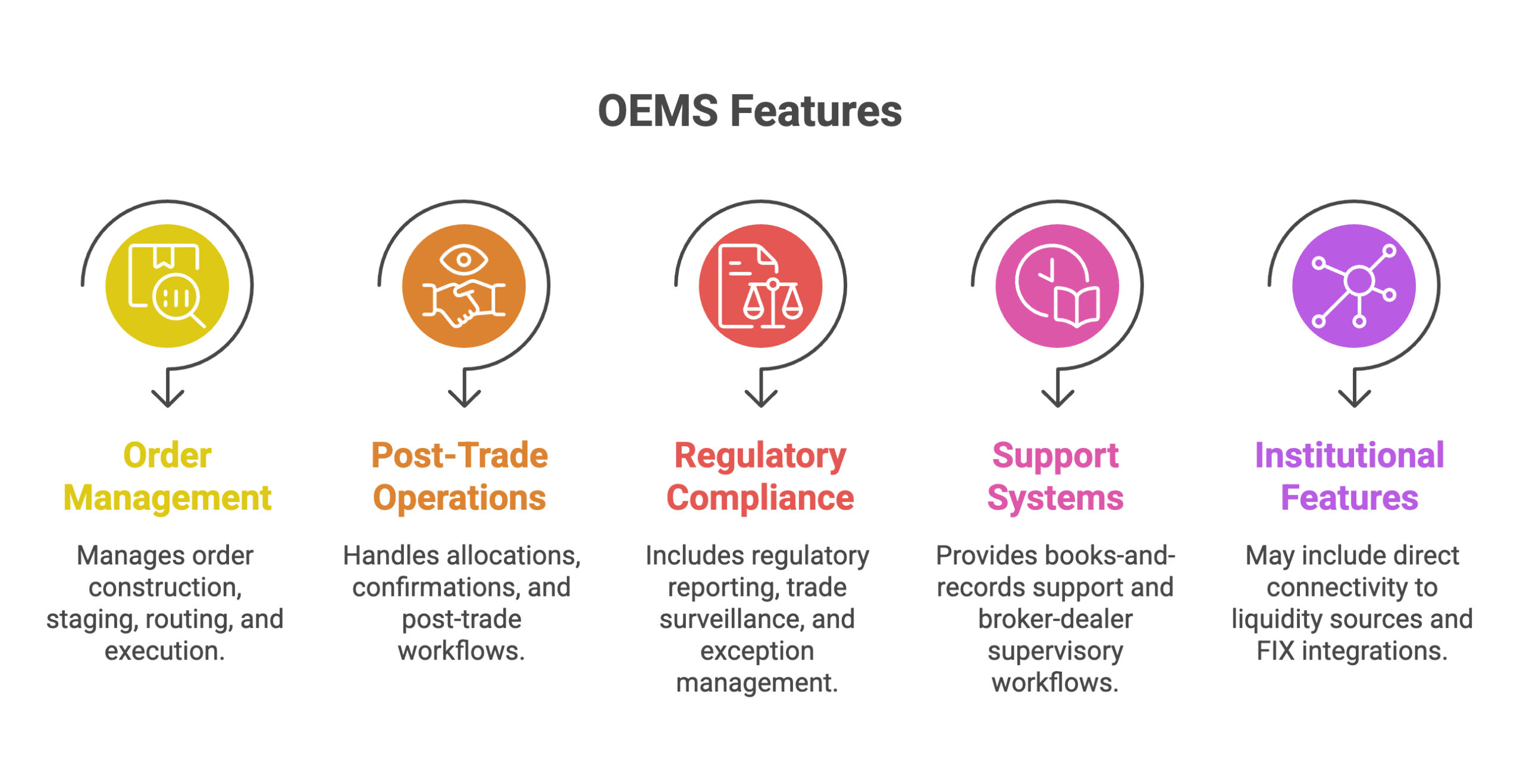

What A “Full Broker-Dealer OEMS” Actually Implies

An OEMS — short for Order and Execution Management System — is the merger of an Order Management System (OMS) and an Execution Management System (EMS). On the buy-side it covers the full journey from order construction through post-trade; on the sell-side, it is the system broker-dealers use to take, stage, route, execute, allocate, confirm, and report client orders at institutional scale.

Industry definitions typically include:

- Order construction, staging, and handling, often with list/program/basket workflows and multi-day order lifecycle tracking

- Direct, low-latency connectivity to dozens or hundreds of liquidity sources — exchanges, ECNs, ATSs, dark pools, market makers — usually over FIX

- Smart order routing, algorithmic execution, and pre-trade analytics

- Full audit trail through post-trade matching, allocation, and confirmation

- Broker commission, fee, and eligibility management

- Real-time risk monitoring and pre-trade compliance checks

When that OEMS is explicitly a broker-dealer OEMS (as opposed to a buy-side OEMS), the bar rises further. A US broker-dealer OEMS is expected to sit inside a regulated workflow that satisfies:

- SEC Rule 17a-3 and 17a-4 books-and-records requirements (blotters, order tickets, customer account records, communications, associated-person records, complaint records, and more — retained for periods ranging from three years to the life of the firm, in WORM-equivalent electronic format after the October 2022 amendments)

- FINRA Rule 3110 supervision (written supervisory procedures, designated supervisors, correspondence review, branch inspections, insider-trading and AML surveillance)

- FINRA Rule 3120 / 3130 supervisory control testing and annual certification

- FINRA Rule 4511 / 4513 recordkeeping and written-customer-complaint files

- SEC Rule 15c3-1 net-capital obligations and 15c3-3 customer-protection / reserve formula compliance where applicable

- Reg BI / Rule 15l-1, suitability, best-execution, Reg SHO, market-access (Rule 15c3-5), OATS/CAT reporting obligations

That is the real promise behind “full broker-dealer OEMS.” It is not just a trading screen; it is a fully instrumented supervisory and recordkeeping system that can survive a regulatory examination.

What A “Brokerage Operations Foundation” Actually Is

A brokerage operations foundation — sometimes called brokerage-as-a-service (BaaS) infrastructure, a white-label brokerage platform, or an embedded-brokerage backbone — is a narrower and deliberately shared layer.

It owns the operational primitives that every regulated trading platform needs, without pretending to be every possible downstream operating model. Typical capabilities include:

- Account and ledger infrastructure — double-entry ledger, reserved cash, locked-FX settlement, restriction handling, GFV tracking

- Funding safety — deposits, withdrawals, instant-deposit gating, settlement work-item modeling, reconciliation hooks

- Order-risk primitives — reservation-first order lifecycle, session-aware order policy, market-status enforcement, degraded-mode fail-fast behavior

- Tenant-scoped supervisory tooling — operations inbox, compliance gateway, elevation and privileged-action patterns, audit-linked actions

- Shared regulatory controls — centralized KYC/AML hooks, restriction workflows, exposure controls

- Contract-first, multi-tenant architecture — DDD/hexagonal boundaries, append-only financial truth, pluggable adapters for clearing, custody, and execution partners

This matches the API-driven, multi-tenant pattern that characterizes most modern brokerage infrastructure providers — where the provider owns the shared regulated plumbing and tenants build differentiated products on top.

Where The Two Categories Diverge

The simplest way to see the gap is to ask: what does the platform own end-to-end, and what does it assume a partner will own?

A foundation owns the shared operational substrate. A full broker-dealer OEMS owns that plus the full trading, execution, surveillance, and supervisory case-management surface required of a registered firm. In clearing-model terms, a foundation maps naturally onto an introducing or fully-disclosed model (where a clearing partner absorbs much of the 15c3-3, custody, and post-trade burden); a full OEMS is what you need when you are operating closer to a self-clearing or omnibus model, where net-capital requirements jump (from $5,000 for a fully-disclosed introducing broker to $250,000 for omnibus, under Rule 15c3-1) and the firm takes direct responsibility for customer-protection, reserve-formula, and back-office completeness.

Pros and Cons: Brokerage Operations Foundation

Pros

1. Faster time to market. Building the entire regulated trading platform stack from scratch typically takes 12+ months and seven-figure budgets. Foundation-style infrastructure lets fintechs, neobanks, and wealth apps go live in weeks rather than years.

2. Platform leverage through multi-tenancy. A foundation solves the hard shared layer once: ledger, reservations, restrictions, audit, supervision. Multiple tenants, multiple operating models, and multiple retail products run on the same substrate, standardizing safety behavior by design.

3. Honest scope. “Foundation” tells the market exactly what is in the box and what a tenant still has to plug in (a clearing relationship, a specific execution venue, a product-specific surveillance rule). That clarity protects trust.

4. Roadmap discipline. Once positioning is correctly scoped to the foundation layer, prioritization becomes cleaner — control-plane hardening, books-and-records maturity, reporting infrastructure, durable event surfaces — rather than surface-level retail polish racing ahead of core operational gaps.

5. Optionality on the operating model. Because a foundation does not bake in a specific broker-dealer workflow, tenants can build an introducing broker, an omnibus model, a prime-brokerage front-end, or an embedded-investing feature inside a non-financial app without fighting the platform’s assumptions.

6. Lower total cost of ownership for the tenant. Shared infrastructure means shared operational cost. Tenants avoid rebuilding ledgers, reservation engines, and audit trails — the most expensive and most error-prone parts of regulated trading.

Cons

1. Not turnkey for a registered broker-dealer. A foundation does not, by itself, satisfy every FINRA/SEC supervisory obligation. The operator still needs WSPs, designated supervisors, AML programs, and often deeper surveillance and case-management tooling layered on top.

2. Dependency surface. Tenants depend on the foundation provider for uptime, upgrades, and regulatory responsiveness. SEA Rule 17a-4(i) makes clear that outsourcing recordkeeping to a third party does not relieve the broker-dealer of ultimate responsibility — so tenants must supervise the provider, not just consume it.

3. Gaps are real and must be honestly disclosed. Areas like full sanctions/OFAC/PEP/EDD workflows, dual-control approval chains, complaint capture per FINRA Rule 4513, exportable books-and-records evidence, deeper supervisory metrics, and full document operations are typically roadmap items in a foundation, not day-one features.

4. Customization ceilings. Multi-tenant architectures trade deep customization for standardized safety. Some tenants will hit limits on what they can configure without contributing upstream or contracting for a dedicated stack.

5. Regulatory ambiguity. The tenant-vs-provider boundary has to be meticulously documented. Regulators (and auditors) will ask who owns what control — a question that foundation providers can answer well only if they have invested in clear contracts, clear scoping, and clear evidence trails.

Pros and Cons: Full Broker-Dealer OEMS

Pros

1. Operational completeness. When it works, a full OEMS is the single pane of glass for a trading desk: order construction, execution, allocation, confirmation, matching, reporting, supervision — with a full audit trail from intake to settlement.

2. Regulatory defensibility at scale. A mature broker-dealer OEMS is designed to stand up to SEC exams, FINRA sweeps, and SRO inquiries. It typically includes surveillance, exception-report generation, communications capture, and the record-retention formats required by the 2022 amendments to Rule 17a-4.

3. Execution quality and connectivity. Institutional-grade OEMS platforms bring hundreds of pre-built FIX connections, algo wheels, smart order routers, and TCA — which are genuinely hard to replicate.

4. Richer supervisory surface. Case management, escalation, alert triage, and compliance gateway behavior tend to be much deeper in a full OEMS than in a foundation.

5. Appropriate for self-clearing or high-touch desks. Firms operating under self-clearing, omnibus, or institutional sell-side models have genuine need for the full stack — and for them, a foundation alone is insufficient.

Cons

1. Expensive and slow to deploy. Even with deployment times trending down (some vendors now quote three weeks on well-understood workflows), a true full OEMS implementation is a multi-quarter project with heavy integration, testing, and certification costs.

2. Opinionated workflows. A full OEMS embeds assumptions about how a broker-dealer operates. Fintechs building embedded or non-traditional experiences often find these assumptions restrictive and end up fighting the system rather than leveraging it.

3. Over-specification for early-stage or embedded products. A neobank adding fractional investing or a wealth app offering a single-venue equities product does not need routing to 140 liquidity sources, basket algos, or program-trading tools. Paying for them distorts unit economics.

4. Overclaiming risk for immature platforms. This is the cautionary tale. A platform that markets itself as a “full broker-dealer OEMS” while still maturing AML case management, dual-control approvals, complaint capture, books-and-records export, or surveillance metrics is setting a bar it cannot clear. The consequences are tangible: buyers expect capabilities that are not present, operators assume more complete supervision than exists, internal roadmap discipline gets distorted by marketing language, and the product ends up being sold ahead of its real control surface. In a regulated domain, that is not just a messaging problem — it is a credibility problem.5. Vendor lock-in and upgrade friction. Heavy, integrated OEMS platforms are hard to replace. Migration projects are measured in years, not quarters, and tenant firms have limited leverage once embedded.

How to Choose Between Them

Choosing infrastructure for a regulated trading platform is not about which category is “better” in the abstract — both are legitimate and both have strong vendors in the market. The decision is about matching the platform to the operator’s regulated scope and product shape.

A few useful tests:

1. What operating model will the firm actually run? Introducing broker with a fully-disclosed clearing partner → a foundation is usually sufficient and more cost-effective. Self-clearing or omnibus broker, or institutional sell-side desk → a full OEMS is typically required.

2. Who owns the supervisory burden? If the operator has its own compliance staff, WSPs, and supervisory control processes, a foundation plus supplemental surveillance tooling often works. If the operator is outsourcing most of the supervisory apparatus to the platform, the platform must genuinely be a full OEMS — or the operator is buying a promise the platform cannot keep.

3. How many tenants or products will run on it? A single brokerage serving one regulated entity may prefer a tightly integrated full OEMS. A platform powering multiple fintechs, neobanks, or regional brands benefits enormously from the multi-tenant discipline of a foundation.

4. How differentiated does the end-user experience need to be? Foundations give more room to build a unique retail or embedded experience on top. Full OEMS platforms tend to standardize the UX and workflow, which is good for institutional desks and limiting for consumer fintech.

5. How mature is the platform actually, today? This is the most honest test. A platform that still has roadmap items in sanctions workflows, dual-control approvals, complaint capture, or books-and-records export should describe itself as a foundation. Calling it a “full broker-dealer OEMS” in that state is overclaiming — and the market, especially sophisticated buyers and regulators, will notice.

Once these questions are answered, vendor evaluation becomes much clearer. The point is not to compare every platform as if it solved the same problem. A fintech building an embedded investing product, a firm operating under an introducing broker model, and a self-clearing broker-dealer will evaluate very different types of infrastructure.

The tables below provide a practical snapshot of selected brokerage infrastructure and OEMS platforms. It is not a ranking or a recommendation. It shows how different solutions map to the two categories discussed in this article — brokerage operations foundation and full broker-dealer OEMS — and what each choice usually means from a technical and implementation perspective.

Brokerage operations foundation

| DriveWealth | Apex Fintech Solutions / AscendOS | |

| Category | Brokerage operations foundation | Brokerage operations foundation |

| Setup / Onboarding Fee | $5,000-$10,000 one-time onboarding and compliance fee, depending on geography and partner licenses. | $20,000-$50,000 one-time fee for integration, compliance review, and ledger setup, depending on complexity and asset types. |

| Platform Fee / Monthly Minimum Pricing | $1,000-$5,000/month fixed infrastructure fee, charged even with 0 clients. | $5,000-$15,000/month for accounts, API, and AscendOS tech stack. |

| Where it can fit | Embedded investing products that need onboarding-to-execution infrastructure without building a separate OMS layer. | Complex investing or broker-dealer platforms needing clearing, custody, trading infrastructure, APIs, SDKs, and real-time ledger capabilities. |

| What this choice means technically | Reduces the need for a separate OMS, but the product becomes tied to DriveWealth’s embedded investing operating model and regional coverage. | Deeper infrastructure coverage, but heavier integration, data migration, reconciliation, and operational dependency on the provider stack. |

Full broker-dealer OEMS

| ION Fidessa | FlexTrade FlexONE / FlexOMS | |

| Category | Full broker-dealer OEMS | Full broker-dealer OEMS |

| Setup / Onboarding Fee | From $50,000 to $250,000+ as a one-time fee, depending on the number of connected exchanges, FIX protocol setup, and compliance configuration. | From $40,000 to $150,000+ as a one-time fee, depending on algorithm customization complexity and integration requirements. |

| Platform Fee / Monthly Minimum Pricing | From $5,000 to $20,000+ per month, as a minimum payment for infrastructure, support, and licenses, regardless of trading volume. | From $4,000 to $15,000+ per month, or $2,000–$4,500 per terminal per month. |

| Where it can fit | Institutional equity trading desks needing integrated execution, order management, middle-office workflows, risk controls, and straight-through processing. | Multi-asset trading teams needing OEMS/OMS workflows, execution management, sell-side automation, custom workflows, and integrations. |

| What this choice means technically | Strong institutional trading depth, but implementation centers on trading desk workflows, FIX/venue connectivity, middle office, and post-trade operations. | High workflow configurability across assets and desks, but more complexity in configuration, integrations, routing logic, and long-term platform governance. |

The value of this comparison is not in choosing the “biggest” platform. It is in narrowing the category before the vendor conversation starts. If the product needs account infrastructure, funding controls, ledger logic, custody/clearing connectivity, and operational workflows, a brokerage operations foundation may be the better fit. If the firm needs institutional order management, execution routing, venue connectivity, middle-office workflows, and post-trade operations, a full broker-dealer OEMS is more likely the right category.

In both cases, the platform should be evaluated against the operating model the firm actually plans to run — not the category label that sounds most complete.

The Positioning Principle

For platform teams, the core principle is simple: claim the category you can actually defend end-to-end.

If the platform owns shared controls, durable records, funding safety, order-risk primitives, and tenant-scoped supervisory tooling — that is a brokerage operations foundation, and that is a strong, differentiated, marketable category. It signals platform leverage, roadmap discipline, and strategic honesty. It leaves explicit room to evolve into deeper broker-dealer-grade capabilities over time.

If the platform has truly completed the full supervisory, surveillance, books-and-records, and execution lifecycle required of a registered broker-dealer, it has earned the right to call itself a full broker-dealer OEMS. The label is accurate, and the market will reward it.

The mistake is claiming the second while only delivering the first. That is where trust erodes — with buyers, with regulators, and with the internal team that has to ship against a promise the product has not yet earned.

In regulated infrastructure, the strongest positioning is not the biggest label. It is the most accurate one.