The ACH Network processed 31.5 billion payments valued at $80.1 trillion in 2023 alone, and real-time payment volumes are climbing fast enough to reshape that picture within a decade. As more financial products demand instant fund movement, the question is no longer whether to support digital payments, but which payment rail fits your use case. Choosing between ACH and RTP affects your customers’ experience, your operational risk, your integration costs, and your fraud exposure. The two systems work differently, cost differently, and serve different business models. This guide breaks down both so you can make that decision with confidence and build payment infrastructure that actually matches your product.

Not sure which rail your product needs? The answer usually comes down to one question: does your user feel the delay?

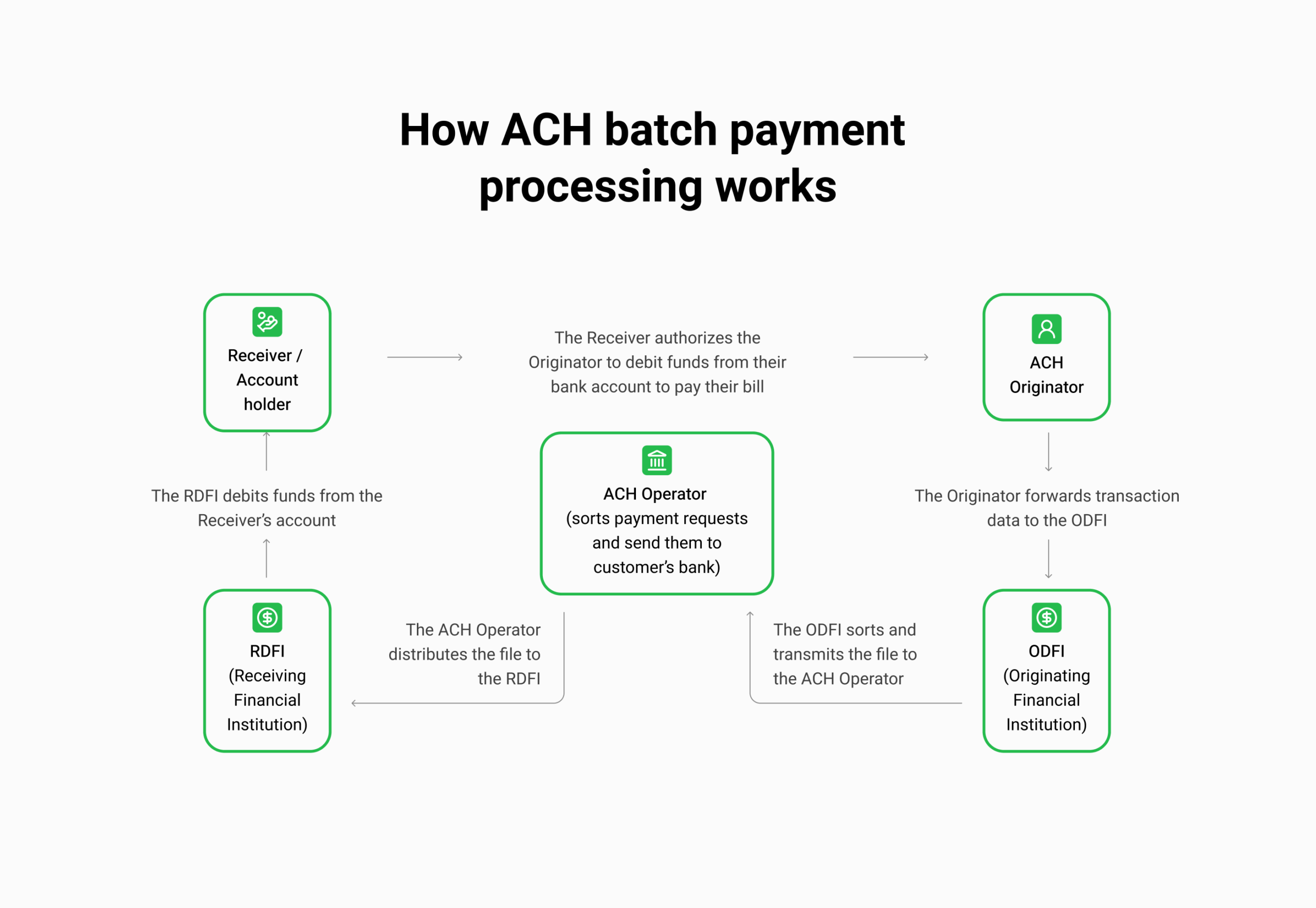

What Is ACH?

ACH (Automated Clearing House) is a batch-based electronic network governed by Nacha that processes transactions in groups at scheduled intervals. It connects virtually every U.S. bank and credit union and handles direct deposits, bill payments, payroll, and B2B transfers. Standard ACH settles within one to three business days; same-day ACH narrows that to within the business day.

A practical example: a company pays 200 employees every Friday via direct deposit. Their bank submits ACH credit entries Thursday evening; Nacha routes them; employees see funds Friday morning. Reliable and deeply embedded in U.S. financial infrastructure. But not instant.

What Is Real-Time Payments?

Real-time payments (RTP) settle transactions within seconds, around the clock, every day of the year including weekends and holidays. In the U.S., two primary rails power this: The Clearing House RTP network, launched in November 2017, and the Federal Reserve’s FedNow service, launched in July 2023. Each RTP payment is processed individually with immediate, irrevocable finality.

A practical example: a gig worker finishes a delivery at 11 PM on Sunday and requests instant payout. With RTP, funds land in their bank account within seconds. No batch window, no waiting until Monday. For platforms where payout speed is a differentiator, that gap is the difference between user retention and churn.

RTP and FedNow are separate rails, not the same system. A bank connected to one is not automatically connected to the other.

RTP vs ACH: Key Differences

Speed is the headline comparison between real time payments vs ACH, but it is rarely the only factor that matters. Businesses evaluating which rail to support need to think across several dimensions: transaction type, user expectations, cost structure, and fraud exposure. Faster is not always better. A same-day payroll run and an emergency insurance disbursement have completely different requirements, and choosing the wrong rail creates real operational and financial problems.

Use Cases

ACH is the backbone of high-volume, predictable payment flows. It dominates use cases where both parties accept a one to three day settlement window and where keeping per-transaction costs low matters more than speed. Common applications include:

- Payroll and direct deposit

- Recurring subscription billing

- Insurance premium collection

- B2B invoicing and vendor payments

- Mortgage and utility payments

- Government benefit disbursements

RTP fits situations where timing is the product itself: instant insurance claim disbursements, on-demand gig worker payouts, same-day loan funding, marketplace seller settlements, and emergency person-to-person transfers. The distinction is not just about speed but about user expectation. When someone requests an instant payout, any delay breaks the promise of the product.

Based on our experience building payment infrastructure for fintech clients, including a B2B invoicing platform processing 100,000+ invoices per month with Dwolla for ACH and Plaid for bank verification, ACH remains the right default for volume-driven, scheduled flows. RTP earns its place when the user experience directly depends on immediacy. If you are building or upgrading a payments product, working with specialized custom ewallet app development services can help you determine the right rail architecture from the start rather than retrofitting it later.

Speed

Standard ACH settles in one to three business days. Same-day ACH cuts that to within the business day using one of three submission windows, but it only operates on business days and has specific cutoff times. RTP settles in seconds and operates 24/7/365 with no batch windows, no cutoff times, and no holiday exceptions.

In the U.S., ACH still dominates by transaction volume because most established financial institutions built their core infrastructure around it over decades. The cost-to-benefit ratio for routine, scheduled transactions remains hard to beat. RTP adoption is accelerating, particularly since FedNow launched in 2023 and extended access to community banks and credit unions beyond the largest commercial institutions.

A direct comparison: a freelancer invoices a client on Friday afternoon. Via ACH, payment clears Monday at the earliest. Via RTP, funds arrive within seconds regardless of the day. For cash-flow-sensitive recipients, that difference directly affects their ability to cover weekend expenses, pay suppliers, or manage working capital.

Same-day ACH is not real-time. It still requires a submission window and only runs on business days — it does not match RTP’s 24/7/365 availability.

Cost

ACH is one of the cheapest electronic payment methods available. Per-transaction fees typically range from $0.20 to $1.50 depending on the provider, volume tier, and whether same-day processing is selected. Large-volume originators often negotiate rates well below $0.50 per transaction.

RTP carries a higher per-transaction fee. The Clearing House charges a flat $0.045 for credit transfers at the network level; end-user pricing reflects provider markup and infrastructure costs, generally ranging from $0.01 to $2.00 per transaction. Unlike ACH, The Clearing House does not offer volume discounts, meaning all institutions pay the same network rate.

For high-volume, low-urgency payments such as monthly payroll or subscription billing, ACH is the clear cost winner. For time-critical disbursements where delay has a measurable business cost, such as a lender releasing same-day funds or an insurer settling a claim, the RTP premium is frequently justified.

Availability

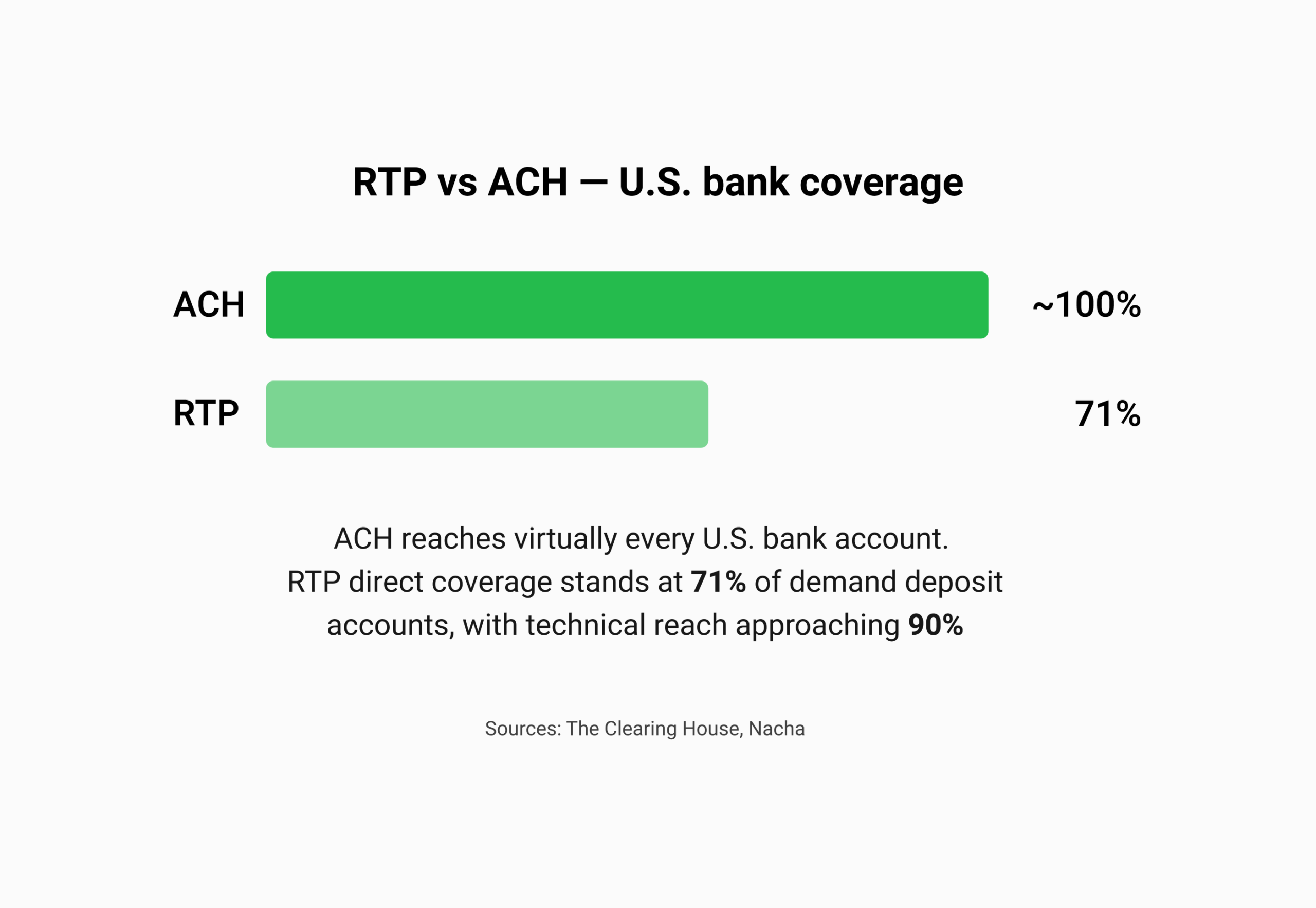

ACH reaches all U.S. bank and credit union accounts, connecting approximately 10,000 financial institutions. It is the universal default for bank-to-bank transfers in the country, which is why it remains the dominant electronic payment method by volume.

RTP availability is growing but not yet universal. The Clearing House RTP network currently reaches 71% of U.S. demand deposit accounts, with technical access available to institutions holding close to 90% of DDAs. FedNow adds further reach, particularly to smaller community banks and credit unions. Together, the two rails cover an expanding share of the U.S. banking system.

If your platform needs to pay out to any U.S. bank account without exception, ACH is the only rail that guarantees universal reach today. If your user base is concentrated with larger institutions and speed is a core product requirement, RTP is viable and increasingly expected.

Fraud Risks

ACH transactions are reversible within defined return windows. On the legitimate side, a duplicate payroll entry or erroneous debit can be recalled before it causes harm. On the fraud side, bad actors can initiate unauthorized debits and dispute them after funds move, or exploit the multi-day settlement window to cycle money out before a return request arrives.

RTP transactions are irrevocable. Once a payment settles, it cannot be pulled back through any automated process. This eliminates return-based fraud but raises the stakes on every authorization decision. If an unauthorized payment goes through, recovery depends entirely on the recipient voluntarily returning funds.

Our data from building payment systems across multiple fintech clients, including a Top-7 U.S. federal credit union platform using Plaid Signal for risk-based funding limits and an e-wallet application built to full AML and PCI DSS compliance standards, shows that real time ACH payments and RTP both require robust pre-transaction verification. The key difference is where your controls need to be strongest: post-settlement dispute management for ACH, pre-authorization risk scoring for RTP.

For RTP, once the payment is sent, recovery depends on the recipient voluntarily returning funds. There is no automated recall mechanism.

RTP vs ACH: Which Should Your Business Choose?

| ACH | RTP | |

| Settlement speed | 1 to 3 days (same-day available) | Seconds, 24/7/365 |

| Bank coverage | ~10,000 institutions, universal | 71% of U.S. DDAs, growing |

| Cost per transaction | $0.20 to $1.50 | $0.01 to $2.00 |

| Reversibility | Yes, returns possible | No, irrevocable |

| Best for | Payroll, subscriptions, B2B billing | Instant payouts, disbursements, on-demand transfers |

Choose ACH when you run high-volume, scheduled payment flows where a one to three day settlement window is acceptable and cost efficiency is a priority. It is the right fit for payroll providers, SaaS subscription platforms, lenders running regular repayment cycles, insurers collecting premiums, and B2B billing systems. The infrastructure is universal, the rules are well understood, and the cost efficiency at scale is unmatched.

Choose RTP when your product’s value is tied to the speed of fund access: gig economy payouts, instant insurance claim disbursements, earned wage access, marketplace seller settlements, or any flow where delay creates direct friction or churn. According to our practice working with fintech clients across payment system builds, platforms that offer instant payouts consistently see stronger user retention than those running standard ACH payout cycles. Many mature platforms run both rails in parallel, routing each transaction automatically through the appropriate channel. Working with experienced banking app development companies in the US can help you architect a dual-rail system from day one.

Conclusion

ACH and RTP are not competing standards where one eventually replaces the other. They are complementary infrastructure layers that serve distinct transaction profiles. ACH is the proven, cost-efficient backbone of U.S. electronic payments, built for predictable, high-volume flows that businesses and consumers have relied on for decades. RTP is the infrastructure layer for products where speed of fund availability is itself a feature, not just a convenience. As FedNow expands and The Clearing House network deepens its institutional reach, the coverage gap between the two systems will continue to narrow. But the underlying logic for choosing between them will not change. Match the rail to the transaction. High-volume, scheduled, cost-sensitive flows belong on ACH. Time-critical, user-facing, experience-dependent flows belong on RTP. Building a payment product that gets this routing right from the start is significantly easier and cheaper than retrofitting it later, and it directly affects both your operating costs and your users’ trust in your platform.