Financial companies have been all over the news for the past few decades or even longer. If you haven’t been living under a rock all this time, you’ve certainly heard of Stripe and how it has revolutionized the payment industry or Robinhood and its quest to make trading accessible to everyone.

FinTech Industry Nonstop Growth Statistics & Facts

However, do you actually know how huge the Financial Services industry is? You might arm yourself with a calculator, start crunching the numbers and arrive at a certain ballpark figure pretty soon. While there is a little doubt in your numerical prowess, most people’s estimates, however, are far off and will never go above a couple hundred billion dollars. The industry is actually much bigger than most people expect it to be: the value of all financial services industry is expected to reach about 26,5 trillion dollars by 2022 which is larger than the GDP of such an economic superpower as the United States and almost twice as large as the Chinese juggernaut economy. With this whopping number, you might think that the industry is operating with maximum efficiency and that there is little room for improvement. You’d be surprised at how much the sector can be improved. There are plenty of inefficiencies in the financial sector. So many, in fact, that the largest banks, insurance companies, and private equity firms lose billions of dollars every year due to technological shortcomings and bureaucratic inefficiencies. That’s precisely when fintech startups jump on the scene and bring about much-needed improvements in the staid and slow-moving industry.

FinTech Startups’ Influence

A few years ago, a fintech trailblazer Robinhood literally turned the complacent and slow-to-change trading industry upside down. Long the haven of the affluent elites, the trading market was harsh on less moneyed newcomers. So were the trading arms of major investment banks or brokerage giants such as Charles Schwab and TD Ameritrade. Unless you had at least a few thousand dollars stashed away to pay a hefty commission for every transaction the traditional players were not for you. The founders of Robinhood saw the opportunity and pretty soon their company changed the industry forever. All of a sudden, anyone with internet access and a few hundred dollars to burn could become a trader. The giants had to adopt the model and scrape off their commissions or risk losing to a bold newcomer started by ambitious Stanford grads. Robinhood is now valued at more than 7 billion dollars reaching this milestone in little more than 6 years, its co-founders are billionaires, and its ascent is only gaining traction.

Along with fintechs like Robinhood that focus on stock trading, other fintech startups are emerging to bring universal access to high credit scores. Some of them offer solutions for individuals, while others are designed to facilitate building business credit scores for companies. StellarFi, founded by unicorn entrepreneur Lamine Zarrad, circumvents outdated credit-scoring models by allowing consumers to build credit using the bills they already pay.

Inspiring Potential of the FinTech Industry for Ambitious Startups

This success of an at-first-sight humble company started by scrappy young entrepreneurs with a clear vision of how they can take on the towering giants serves as a clear example of how much room for improvement there is in the financial industry. It also showcases that fortunes can be made if you have the right idea that could help streamline the processes in the industry that has become so big that it finds it hard to keep abreast with the latest technological innovations. Few spheres hold as much potential for striking it big and improving the world along the way, which is something most young entrepreneurs aspire to, as Fintech.

This potential, however, is far from being unnoticed. More and more of the world’s best and brightest ones see the allure of taking the path of a fintech entrepreneur who, instead of joining the financial industry, creates a company that will disrupt it and keeps the high-paid and complacent bankers sitting in the towering skyscrapers of the London’s City, New York’s Wall Street, and Hong Kong’s financial district up at night. The graduates of Oxford, Harvard, or Tsinghua who would normally go on to obtain highly coveted investment banking and finance jobs are instead opting to start their own companies and flock to the technological and venture capital hubs of Silicon Valley and Shenzhen.

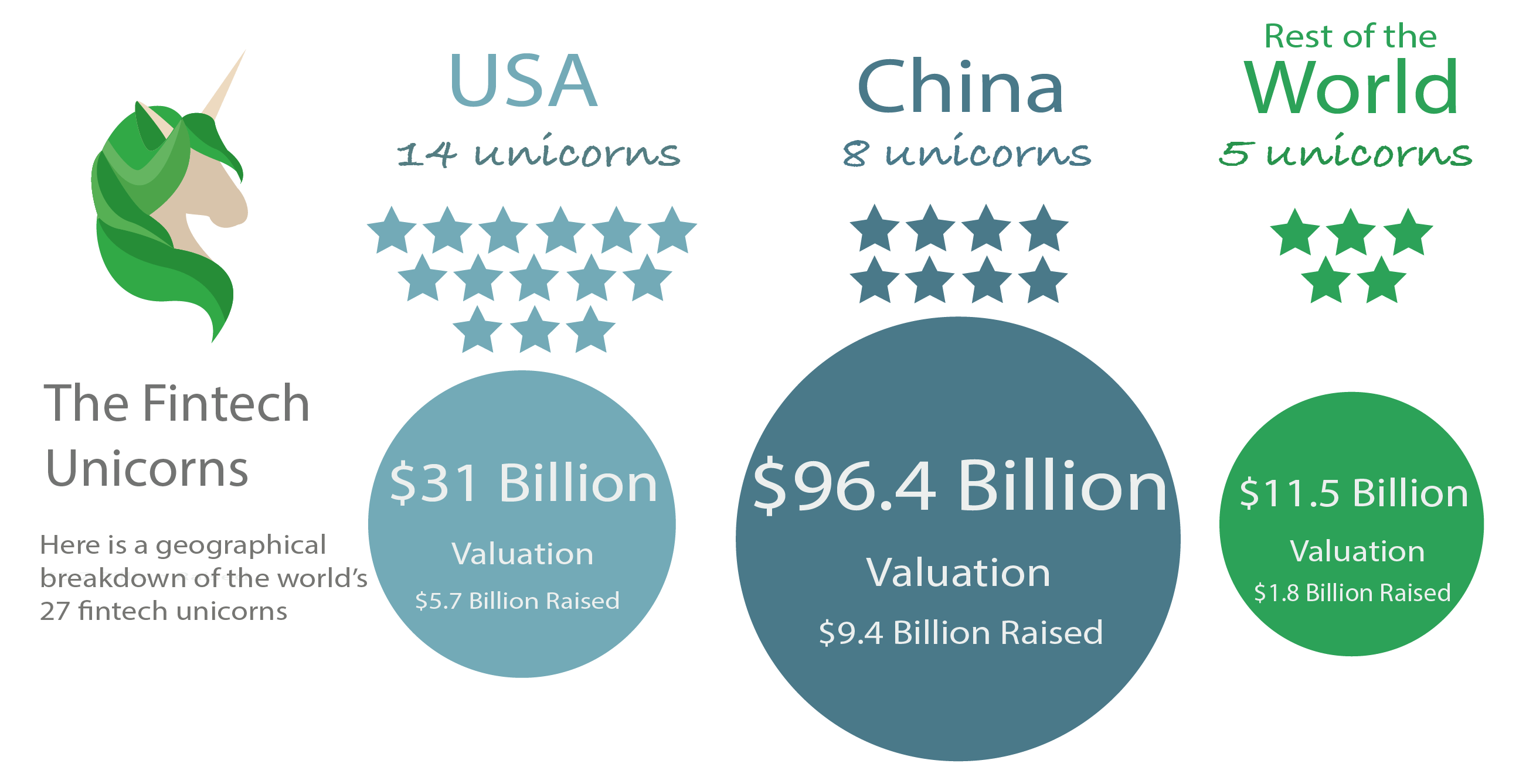

FinTech Unicorns Statistics

This entrepreneurial drive is certainly reflected in the value of fintech unicorns that have emerged all over the world in the last decade. Their combined valuation has reached a massive 147 billion dollars and continues to grow by leaps and bounds each passing year. The bulk of the industry, contrary to expectations, is concentrated in China buoyed by the tech-savvy and ambitious government and tech giants such as Alibaba and Tencent, fintech has enjoyed truly rocket growth. The United States and Europe are no slouches though. Some of the most disruptive and successful fintech unicorns were born in California surrounded by the palms and miles of sandy beaches, in strict and rainy London, or in Stockholm during its perennially dark winters.

These FinTech unicorns are far from being a uniform bunch, however. In fact, they are as varied as the financial industry itself.

FinTech Giants

The payment giants of Ant Financial (Alipay), Stripe, and Klarna are for many outsides of the industry the epitomes of the rising power of fintech. As often as the word “disruptive” is thrown around, this word is probably apt to describe these juggernauts. All of them are changing the industry, all of them are valued at billions of dollars, and all of them keep rising fast conquering new niches either by buying existing companies or expanding their expertise. Alipay, for instance, is responsible for the near elimination of cash transactions in China. In fact, the first thing that surprises a cash-carrying European in China is how few Chinese people have actually seen their money and how everybody, from an old lady selling vegetables in the Shanghai market to a taxi driver in a small town, tucked away in the far west Sichuan province has an Alipay account that enables paying with a smartphone by merely scanning a QR code. Stripe has been equally disruptive across the ocean. Seeing how cumbersome and expensive it can be to accept payments online, Stripe’s founders decided to bank on their product’s simplicity, and it panned out. Stripe has now become one of the largest payment processors in the United States and, armed with a stash of cash it has earned in this lucrative market, it is now gearing up for a major international expansion.

With a fragmented market that comprises hundreds of lenders espousing sometimes drastically different policies, the consumer and small business loan market proved to be another fertile ground for an unstoppable fintech expansion. In a matter of several years, several strong unicorn contenders emerged to rival the more established players. One such company is the Atlanta-based Kabbage which just recently raised a hefty 250 million from a slew of VC companies and institutional investors. Determined to eliminate the numerous hoops small businesses have to jump through to obtain funding, Kabbage introduced an AI-based lending platform that proved to be enormously popular in the United States. The unicorn is now voraciously expanding overseas bringing needed-and long overdue change to the industry leaving some of the traditional players who are unwilling to adapt to bite the dust.

To Sum It Up

Rest assured though, traditional players are still huge, and they are not going to give up so easily. Slowly, but markedly established companies are starting to pay attention to the Fintech wave that is threatening to dethrone some of them and occupy niches that some of those companies have held for decades. Yet, the size of these companies plays against them: they are slow to react. There are so many opportunities to revolutionize the financial industry that stemming the tide of new fintech startups is likely to prove impossible.

As you can see, there is a lot of work to be done in fintech software development right now to meet the demand of software development companies that can help turn your brilliant fintech idea into a polished and wholesome product ready to conquer the world. Traditional companies will have to adopt the new rules and make more and more online services available as well as adopt all the latest innovative processes that startups thrive on. Fun times full of change and uncertainty are ahead in the fintech industry as startups and established players duke it out over market domination. Fintech has never been more interesting to keep your eyes on.

Liked the article? Rate us

Average rating: 0 (0 votes)